Consequently, what is FIFO and LIFO example?

FIFO (“First-In, First-Out”) assumes that the oldest products in a company's inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company's inventory have been sold first and uses those costs instead.

Beside above, what is the FIFO method? FIFO stands for “First-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The FIFO method assumes that the oldest products in a company's inventory have been sold first. The costs paid for those oldest products are the ones used in the calculation.

Subsequently, one may also ask, what is difference between FIFO and LIFO?

Key Differences Between LIFO and FIFO In LIFO, the stock in hand represents, oldest stock while in FIFO, the stock in hand is the latest lot of goods. In LIFO, the cost of goods sold (COGS) shows current market price while in the case of FIFO the cost of unsold stock shows current market price.

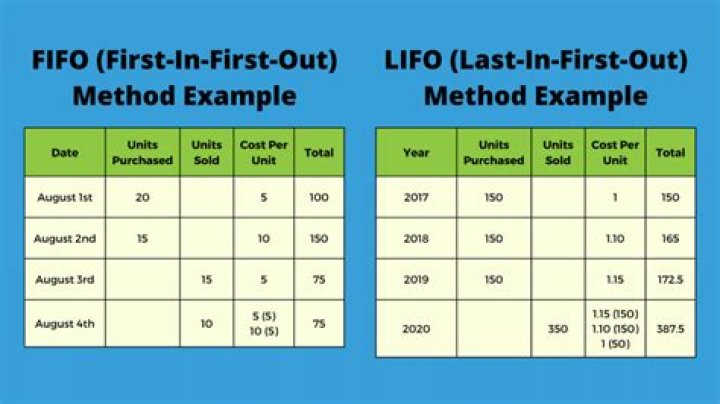

What is LIFO example?

LIFO stands for “Last-In, First-Out”. It is a method used for cost flow assumption purposes in the cost of goods sold calculation. The LIFO method assumes that the most recent products added to a company's inventory have been sold first. The costs paid for those recent products are the ones used in the calculation.

What is FIFO example?

Under the FIFO method, the earliest goods purchased are the first ones removed from the inventory account. For example, in an inflationary environment, current-cost revenue dollars will be matched against older and lower-cost inventory items, which yields the highest possible gross margin.Why is FIFO used?

The FIFO and LIFO Methods are accounting techniques used in managing a company's stock and financial matters. They help a company determine the value of their stock, raw materials, etc. They are used to manage cost flows assumptions related to stock and stock repurchases (if purchased at different prices).Where is LIFO used?

The LIFO (Last-in, first-out) process is mainly used to place an accounting value on inventories. It is based on the theory that the last inventory item purchased is the first one to be sold. LIFO method is like any store where the clerks stock the last item from front and customers purchase items from front itself.Can a company use both LIFO and FIFO?

U.S. accounting standards do not require that the method mirrors how a business sells it goods. If a business sells its earliest produced goods first, it can still choose LIFO. FIFO is the most used method by major U.S. methods, but LIFO is a close second.Who uses FIFO?

Just to name a few examples, Dell Computer (NASDAQ:DELL) uses FIFO. General Electric (NYSE:GE) uses LIFO for its U.S. inventory and FIFO for international. Teen retailer Hot Topic (NASDAQ:HOTT) uses FIFO. Wal-Mart (NYSE:WMT) uses LIFO.Is FIFO allowed under GAAP?

Unlike the inventory reporting rules under the International Financial Reporting Standards, or IFRS, the generally accepted accounting principles, or GAAP, do not require companies to use the first-in first-out, or FIFO, method exclusively.What are the advantages of FIFO?

Advantages and disadvantages of FIFO The FIFO method has four major advantages: (1) it is easy to apply, (2) the assumed flow of costs corresponds with the normal physical flow of goods, (3) no manipulation of income is possible, and (4) the balance sheet amount for inventory is likely to approximate the current marketWhy LIFO is not allowed?

One of the reason that LIFO is not allowed because reduction in tax burden under inflationary economies. This can happen because LIFO assumes that inventory will be consumed in the production process. The main reason for excluding the LIFO is because IFRS shifted its focus on balance sheet instead of income statement.Why do we use LIFO and FIFO?

Reason for Using LIFO (The higher cost of goods sold means lower net income and lower taxable income than FIFO.) If the company had matched the old low costs using FIFO, the company would show a greater profit that was partly caused by merely holding some old inventory items.What is LIFO FIFO and average cost?

First-In-First-Out & Last-In-First-Out. Inventory can be valued by using a number of different methods. The most common of these methods are the FIFO, LIFO and Average Cost Method. It is calculated by dividing the total number of units you have on hand by the total cost of goods.What is the meaning of LIFO?

Last In, First Out (LIFO) Definition: An accounting method for inventory and cost of sales in which the last items produced or purchased are assumed to be sold first; allows business owner to value inventory at the less expensive cost of the older inventory; typically used during times of high inflation.Is FIFO or LIFO better?

First, remember this: Higher-cost inventory = lower taxes. Lower-cost inventory = higher taxes. Since prices usually increase, most businesses prefer to use LIFO costing. If you want a more accurate cost, FIFO is better, because it assumes that older less-costly items are most usually sold first.What is mean by LIFO?

LIFO is the acronym for last-in, first-out, which is a cost flow assumption often used by U.S. corporations in moving costs from inventory to the cost of goods sold.Is LIFO allowed in India?

IFRS which is followed in most of the countries does not allow LIFO accounting. In India, as per Revised AS 2, LIFO method of inventory is not permitted and companies would have to account inventory based on either FIFO or weighted average cost method.What is the full meaning of FIFO?

FIFO. "FIFO" stands for first-in, first-out, meaning that the oldest inventory items are recorded as sold first but do not necessarily mean that the exact oldest physical object has been tracked and sold. In other words, the cost associated with the inventory that was purchased first is the cost expensed first.What are the 4 types of inventory?

Generally, inventory types can be grouped into four classifications: raw material, work-in-process, finished goods, and MRO goods.- RAW MATERIALS.

- WORK-IN-PROCESS.

- FINISHED GOODS.

- TRANSIT INVENTORY.

- BUFFER INVENTORY.

- ANTICIPATION INVENTORY.

- DECOUPLING INVENTORY.

- CYCLE INVENTORY.