Generally, homeowners may deduct interest paid on HELOC debt up to $100,000. Beginning in 2018, taxpayers may deduct interest on just $750,000 in home loans.Then, is Heloc interest tax deductible 2019?

Under the new law, home equity loans and lines of credit are no longer tax-deductible. However, the interest on HELOC money used for capital improvements to a home is still tax-deductible, as long as it falls within the home loan debt limit.

Similarly, can home equity loan interest be deducted in 2018? According to the advisory, the new tax law suspends the deduction for home equity interest from 2018 to 2026 — unless the loan is used to “buy, build or substantially improve” the home that secures the loan. Beginning this year, taxpayers may deduct interest on just $750,000 in home loans.

In respect to this, can you deduct interest on a Heloc?

The deduction amount includes the interest you pay on your mortgage, home equity loan, home equity line of credit (HELOC) or mortgage refinance. 15, 2017, you can deduct interest on $1 million worth of qualified loans for married couples and $500,000 for those filing separately for the 2018 tax year.

Is a Heloc considered taxable income?

HELOCs and second mortgages will no longer be deductible if the loan proceeds are used to pay for personal items, including college tuition, vacations, credit card debt, student loan debt, a vehicle or clothing; the interest paid on that amount will not be deductible. These are deductions, not tax credits.

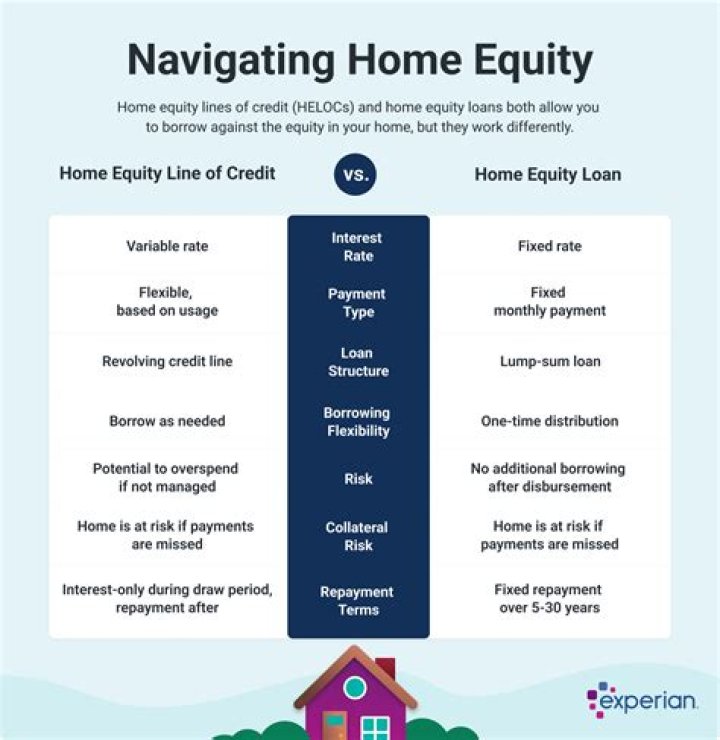

Which is better Heloc or home equity loan?

A home equity loan is best if you prefer fixed monthly payments and know exactly how much money you need for a financial goal or home improvement project. On the other hand, a HELOC is a better fit for financial needs spread over time, or if you want flexible access to your equity that you can pay off quickly.What are the disadvantages of a home equity line of credit?

Below are three disadvantages you'll want to seriously consider before you commit to a HELOC. - Possible Foreclosure: When a lender grants a home equity line of credit, the borrower's home is secured as collateral.

- Risk of More Debt: Among the biggest problems associated with HELOCs is the potential to rack up more debt.

How is Heloc interest calculated?

Because the balance of a HELOC may change from day to day, depending on draws and repayments, interest on a HELOC is calculated daily rather than monthly. On a 6% HELOC, interest for a day is . 06 divided by 365 or . 000164, which is multiplied by the average daily balance during the month.Is cash payment a tax?

Even though you're paid in cash, you still need to pay Social Security and Medicare taxes. If you are an employee, your Social Security and Medicare taxes should have been withheld from your payments. This is referred to as FICA. However, as these are cash payments, this may have not happened.Is Heloc a good idea?

A HELOC works similar to a credit card because it gives you a credit limit and you can take out money in increments rather than a home equity loan, which gives you all the money at once. HELOCs can be a great option when you need to pay for college, medical expenses and home improvement projects.Should I pay off my mortgage with a Heloc?

The HELOC strategy is at its heart a debt strategy. You're using a credit card and a HELOC to pay off your mortgage. In the short run at least, that means replacing long-term debt with short-term debt. The only way to truly get out of debt is by paying it off out of your income or other assets.What is the standard deduction for 2019?

$12,200

How does Heloc affect credit?

Because it has a minimum monthly payment and a limit, a HELOC can directly affect your credit score since it looks like a credit card to credit agencies. Since a HELOC has a variable interest rate, payments can increase when interest rates rise and decrease when interest rates fall.Does unused Heloc affect credit score?

Do Unused Credit Lines Hurt Your Credit Score? Unused lines of credit typically improve your utilization rate, which would improve your credit score. However, HELOCs are a type of revolving credit, just like a credit card.Can you get a fixed rate on a Heloc?

Traditionally, if you wanted to borrow against the equity in your home, you could either get a fixed-rate home equity loan or draw money against a home equity line of credit (HELOC), a closed-end line of credit with a variable interest rate. Now there's a third choice: the HELOC fixed-rate option.Can I pay off Heloc early?

The HELOC offers you access to a specified amount of money, but you do not have to use any of it. At any time, you can pay off any remaining balance owed against your HELOC. If you pay off your HELOC early and don't want to pay the annual fees, closing the line of credit can be a good idea.Can you refinance a Heloc loan?

Homeowners can refinance their HELOCs into a new home equity line of credit, one starting over with a new draw period and the lower monthly payments that come with it. Or they can refinance both their HELOC and the balance of their principal mortgage into a single home loan.What is an interest only Heloc?

Interest-Only HELOCs Explained. But with an interest-only HELOC, you pay only monthly interest during that draw period, minimizing the size of your monthly payments. You're only responsible for the repayment of principal when the draw period ends.Is second home mortgage interest deductible in 2018?

As of the 2018 tax year, you can deduct interest on $750,000 in home loans, including mortgages. However, keep in mind that this figure is the combined total of all loans used to buy, build, or improve your primary and second homes.Is interest on a 2nd mortgage tax deductible?

Taxpayers can deduct the interest paid on first and second mortgages up to $1,000,000 in mortgage debt (the limit is $500,000 if married and filing separately). Any interest paid on first or second mortgages over this amount is not tax deductible. The marginal Federal tax rate you expect to pay.Can you write off 2nd mortgage interest in 2018?

Beginning in 2018, taxpayers may only deduct interest on $750,000 of qualified residence loans. The limit is $375,000 for a married taxpayer filing a separate return. The limits apply to the combined amount of loans used to buy, build or substantially improve the taxpayer's main home and second home.Can you claim line of credit interest on taxes?

You may take up a line of credit, get a loan or put expenses on your credit cards. You can deduct the interest charged on these funds from the business income, and if the business takes a loss, from any other income you may have. All interest your business pays to finance its operations is usually deductible.